Keeping yourself, and your business, safe |

Dear *|FNAME|*,

This month we're covering some cautionary tales and advice to help keep you safe, as well as any business dealings you might have. Scams (avoiding them), tax (not avoiding it), and employment arrangements (avoiding them going awry).

But in more positive news, first it's our pleasure to welcome another new face to the team.

|

|

|

|

|

|

Welcome Terena Te Whaiti! |

|

Following Claudia Leighs' recent arrival at Canterbury Legal, our litigation team continues to grow with our new litigation lawyer, Terena Te Whaiti.

Terena joined us in October, bringing a strong background in multiple types of litigation, including a stint in Australia.

She's all about finding pragmatic, successful resolutions for her clients, so we're pleased she can now offer those to you. Learn more about Terena. |

|

|

|

|

|

|

Are you being scammed? |

|

Occasionally clients come to us for help after they suspect they’ve been scammed.

Sometimes there’s a practical solution we can provide. But more often than not, by the time they reach our office, it’s simply too late.

So if we can’t be your ‘ambulance at the bottom of the cliff,’ hopefully we can help keep you away from that metaphorical cliff in the first place.

The scam landscape

If you think talk of scams sounds like fearmongering… then you may have a well-attuned radar for spotting a scam! Many scams operate on exploiting people’s fears, using messages of urgency and opportunity.

But they’re also usually divorced from facts. So here are some of those.

CERT NZ responded to 1091 scam and fraud incidents in the first half of this year, up 30 percent from the same period in 2021. Scams affecting individuals cost $3.2 million between April and June alone. CERT NZ also responded to 2486 phishing and credential harvesting attacks, up a massive 96 percent. Scam complaints made to the Banking Ombudsman increased by 63 percent in 2021/2022 over the previous year. 87 percent of respondents to a Westpac survey thought they had received a scam email, text or phone call in the past six months. And given scams are intended to go unnoticed, the other 13 percent probably received one, too. So why the increase? And why do scammers seem to be experiencing greater success?

Banking Ombudsman Nicola Sladden attributes at least some of it to a similar rise in scammer sophistication. They impersonate organisations such as banks or telecommunications companies, seeking money or account details. Or they even impersonate friends or family members on social media.

Westpac’s head of financial crime Mark Coxhead shares that view, adding that scammers often use personal information they find online, and call from phone numbers that appear legitimate. In one case, a scammer was able to use a Westpac customer’s name, phone number and credit card details to trick them into divulging even more information.

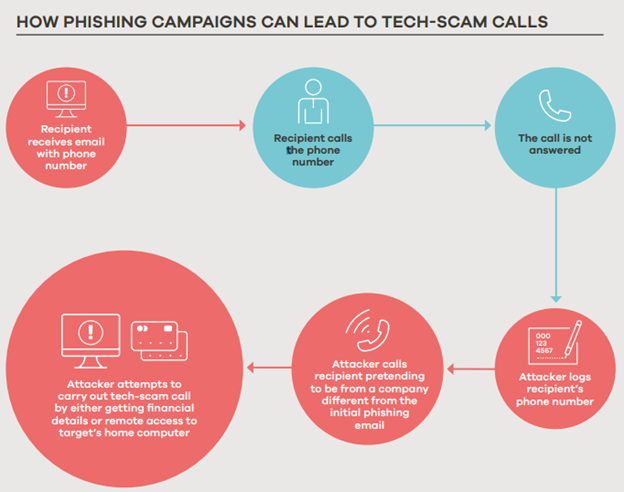

CERT NZ director Rob Pope says phishing attacks (scams to persuade people to share personal information) work as gateways to other scams. Scammers using them might use authoritative language or play on people’s emotions, such as invoking the threat of a fine, or, earlier this year, fake relief efforts for Ukraine. And while technology can make systems more secure from hacking or similar attacks, the people with legitimate access to those systems are still prone to being exploited or deceived.

CERT NZ’s Q1 2022 report provides a good illustration of how phishing can lead to a scam.

|

|

So what can you do to stop being scammed?

It’s unlikely any of us can completely avoid scam attempts. But we can reduce the chance we fall prey to them.

If it feels too good to be true, it probably is. That’s the advice from Mark Coxhead at Westpac, and it remains as true as ever. If it feels too bad to be true, it probably is. Remember, scams prey on our fears, too. That warning of a fine, penalty or security risk might be just as imaginary as an unexpected windfall. Where possible, set up two-factor authentication. This includes your internet banking. And never give a two-factor authentication code to anyone else. Beware of unusual payment methods. Scammers may ask you to pay using cryptocurrency or gift cards. That’s unlikely to happen with a legitimate organisation. Don’t feel pressure to pay straight away. If it’s a legitimate expense or bill, you should be given time. If someone is demanding payment immediately, it’s a red flag. Don’t give out passwords or PINs over the phone or email. This goes double if they were the ones who called or emailed you in the first place. Banks will never ask for this information. Beware of links in texts or emails. It’s easy to make fraudulent links appear legitimate. Make sure email addresses match the organisation purporting to send them. Though even these can be falsified. Research investments before taking action. If someone cold calls you about an opportunity, they’re breaking the law. And anyone promoting an investment opportunity should provide full information in writing, including legitimate physical contact details. And remember the first tip in this list: if guaranteed high returns with no risk were so commonplace, we’d all be rich. Be careful about what information you share online. Your social media accounts and posts are excellent sources of information about you. So are registration forms you fill in for supposedly legitimate businesses. While privacy laws mean most organisations cannot share this information legally, this isn’t always the deterrent it should be. This kind of information can be used to contact you, and deceive you into giving over even more. If in doubt, call the organisation using a phone number you know is legitimate. If it’s a bank, it will be on the back of your bank card. If another organisation, it might be on past legitimate correspondence, or accessible via the 018 directory service.

And if you think you’ve already been scammed…

Notify your bank, if you think any of your accounts are at risk, or you think you’ve made a payment to a scammer. Report it to CERT NZ. They may also be able to refer you to other organisations you should contact. And even if they are unable to resolve things for you, the information could help prevent others from suffering the same fate.

And while we may not be able to be your ambulance at the bottom of a cliff, we are always here to provide you with an objective perspective and guidance, particularly when you are entering into any contractual arrangements. Never hesitate to call or email us.

|

|

|

|

|

|

Employment Court holds four Uber drivers are employees, not contractors |

The question of whether people working in the “gig economy” are employees or contractors has been answered in different ways over the past couple of years. A recent Employment Court decision adds some more certainty to the matter, though it will likely be appealed.

Chief Judge Christina Inglis held that four drivers of Uber’s rideshare and Uber Eats services were indeed employees of the company, rather than contractors, in contrast to a 2020 decision by the same court.

In this case, Chief Judge Inglis held it was necessary to look at all relevant matters of the situation, and not just what the parties (Uber and the drivers) intended the relationship to be.

Uber argued that it acted only as an intermediary, and the way the drivers conducted their work, and the control exercised over it did not amount to an employer/employee relationship.

But the Court said many factors of the relationship did point to such a relationship. These included:

Uber’s sole power to control prices, service requirements, terms, and guidelines the restriction on drivers from forming relationships with riders the restriction on drivers to organise substitute drivers to work on their behalf the system of ratings and incentives Uber applied.

With this in mind, the Court said Uber appeared to run a transportation business, not just an app, and that the drivers worked for that business.

The significance is that employees and contractors have different rights and protections. If someone is held to be an employee, the company said to be employing them will need to meet different responsibilities and obligations. For Uber, that could have a significant impact on how they run their business—not to mention other companies such as couriers and cleaning companies, who sometimes work with who they deem to be contractors.

The decision technically applies only to the four drivers involved. However, the Chief Judge Inglis added a final comment to her judgement that decisions like this can apply more broadly when the arrangements in question apply to other people working for or on behalf of the business. Given the four drivers had the same working arrangements as the rest of Uber’s driving force, it is likely to be relevant to all of them as well.

So if you run a business, or work as a contractor, take note. No matter what you write in a contractual arrangement, the reality of the work and relationship is what really matters. Consider your work carefully.

|

|

|

|

|

|

Pepsi parent’s IRD bill not looking so sweet |

|

The company behind Pepsi’s New Zealand operations is facing a hefty bill after the Supreme Court ruled it engaged in tax avoidance.

Frucor Suntory, which also owns the V, Just Juice and Fresh Up brands, is now liable for $3.7m in shortfall penalties—as well as IRD’s costs of $45,000 plus expenses.

The case related to a 2003 funding deal. Frucor claimed $66m it paid to Deutsche Bank was interest, and therefore a valid tax deduction. IRD argued that the actual interest paid was only $11m, and the remaining $55m was simply repayment of the loan principal.

Previously, the High Court held that it was not tax avoidance. The Court of Appeal disagreed, saying it was tax avoidance, but Frucor was not required to pay shortfall penalties.

The Supreme Court’s decision turned on a two-step rule from a 2008 case, Ben Nevis Forestry Ventures Ltd v Commissioner of Inland Revenue.

Whether the use of a tax provision was within its intended scope. Whether in light of the entire arrangement, the taxpayer’s use of the provision was outside Parliament’s intention when it enacted it.

The Court ruled unanimously that the provision was used within its intended scope. But the majority ruled the second step was not met. The provision allowing tax deduction was intended to apply to interest only, and Frucor used “contrived and artificial” arrangements to try to apply it to a principal repayment.

The majority also held shortfall penalties were allowed, as Frucor’s application of the provision was not “about as likely as not to be correct”—the test from the Tax Administration Act 1994.

What can those of us who are not engaging in multi-million dollar funding deals learn from this? Take care with your tax and contractual arrangements. While there are many legitimate ways to structure things to reduce tax liability, they need to align with what the law intended. |

|

|

|

Monthly Housing Update |

House prices continue to trend downward in Christchurch, according to CoreLogic’s October report. The number of sales is also well down. According to REINZ, 741 homes sold in Canterbury in October 2022, down 33.7% from the same month last year; 452 in Christchurch, down 36.4%.

Add to that the news that the number of Q3 first home purchases was the lowest Q3 figure since 2011, and things might seem a little bleak for all concerned.

But there are glimmers of optimism. While first home purchases were lower than normal in Q3, they represent an increasing chunk of the market at 24%, versus the long-term average of 22%. The size of October’s Christchurch price drop is smaller than the monthly average for the quarter: 0.2% versus 0.7%. And looking back a year, house prices are still up 8.8%. The situation here is better than elsewhere in the country.

So there are opportunities out there, whether you’re buying or selling. But given that the market is a little tougher to navigate at the moment, we’re making it easier for you if you want to buy or sell before Christmas. We’ve taken 20% off all our conveyancing fees. Register now, or call for advice. |

| Register for our conveyancing deal - 20% off |

|

|

|

|

|

Thanks *|FNAME|*.

Thank you for reading this month! We’ll be back for our final edition of 2022 in December. But until then, as always, we’re just an email or phone call away.

Regards,

Clive, Grant and the Team at Canterbury Legal |

|

|

|

|

|

Legal Tip💡 |

Before entering into any transaction involving large sums of money, seek professional third-party advice. It’ll help you see the situation more clearly, understand the risks, and perhaps avoid an unwanted outcome. |

|

|

|

|